Why

Investing in both traditional and alternative investments is fast becoming the modern way to prudently grow and protect your wealth.

Public equities and fixed income securities, commonly referred to as “stocks and bonds”, constitute traditional investments.

Alternative asset classes include almost anything else, most commonly real estate, private debt, private equity, infrastructure and absolute return strategies.

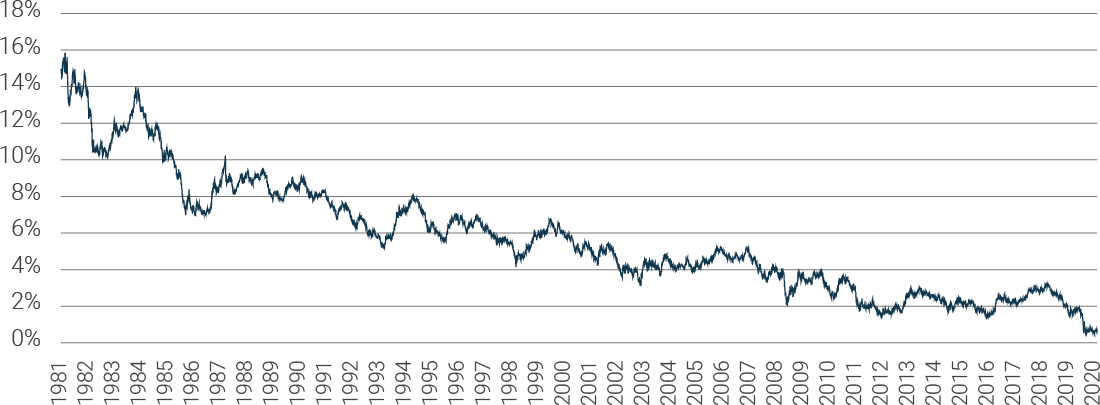

So what is wrong with the status quo? A typical traditional portfolio is 60% public equities and 40% fixed income. Lets look at fixed income first, i.e., bonds. Bond yields have gone from the high teens in 1981, to near zero today, making the asset class unable to meet the income investment objectives of many investors.

10-Year Treasury Constant Maturity Rate, Percent, Daily, Not Seasonally Adjusted

Source: FRED (Federal Reserve Economic Data)

Public Equities, or Stocks, on the other hand, while historically have been a good source of excess return, are also prone to extreme volatility, and can have long periods where the broader market as measured by the index does not earn any positive return. As such, it is generally not an appropriate or desirable asset class to have all of one’s wealth in one volatile asset class such as public equity. Bear markets can take long periods of time to recover and the drawdowns can be very significant, sometimes more than 50% on a peak to valley basis. For example, the bear market of 2008, the drawdown period took seven years for the indexes to regain their pre-bear market levels. Also, the ability to diversify within public markets has become increasingly difficult as equities across countries and sectors have become highly correlated, i.e., They move in the same direction at same time. Adding more equities to your portfolio is unlikely to improve diversification, or reduce risk in a meaningful way, and instead, merely converges the portfolio return to that of the broader index.

RETAIL VS. INSTITUTIONAL APPROACH TO ASSET ALLOCATION

Status Quo Canadian Retail Asset Allocation

- Canadian Equity: 60%

- Fixed Income: 40%

Institutional Approach to Asset Allocation

- Canadian Equity: 30%

- Fixed Income: 15%

- Real Estate: 20%

- Private Debt: 15%

- Private Equity: 7.5%

- Absolute Return Strategies: 7.5%

- Infrastructure: 5%

Source: Internal

Note: Portfolios are hypothetical, for illustration purposes only. Actual retail and institutional portfolios will vary widely

However, adding other asset classes with strong return profiles, that are uncorrelated, or less correlated, with stocks and bonds, can add proper diversification to reduce volatility and potentially downside risk. Alternative

asset classes like real estate, private debt , private equity, infrastructure and other have historically had distinctly different return streams than stocks and bonds, and thus can smooth out the return profile of the resulting portfolio to achieve a better outcome than the traditional 60-40 approach. To put it a different way, adding non-correlated alternative assets can push out the efficient frontier and help a portfolio achieve a higher return with the same level of risk, or the same return with a lower level of volatility and risk.

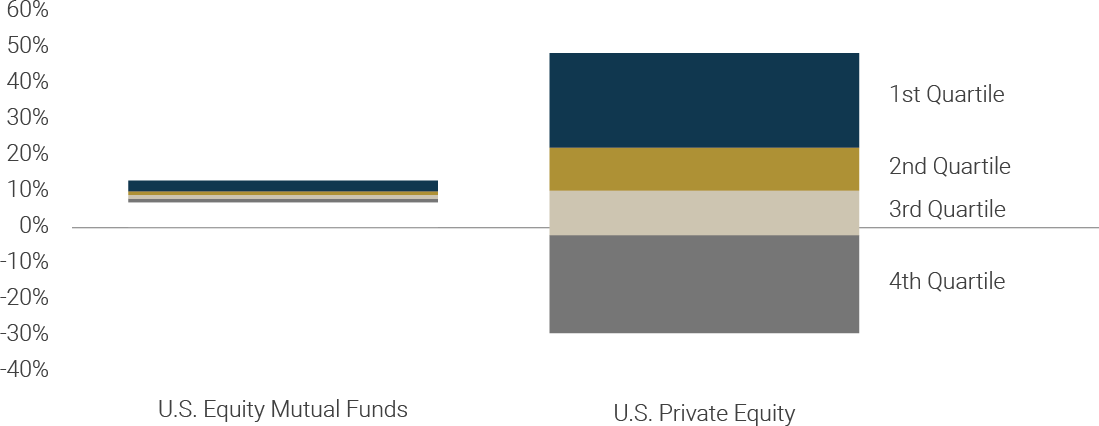

SKILLED ACTIVE MANAGERS HAVE A GREATER OPPORTUNITY TO OUTPERFORM IN PRIVATE MARKETS

5-year annual returns from U.S. Private Equity Funds and U.S. Mutual Funds by Performance Percentile, 2013–2018, %

Source: Morningstar; Burgiss

It is important to note that alternative asset classes are not necessarily more risky, or less risky than traditional ones. All investments have risks, but it is precisely the process of building a portfolio of different

risks that protects an investor from systemic decline (bear market) of the value of their portfolio. Modern portfolio theory, which has been widely accepted academically for more than 50 years, tells us that adding an asset to a portfolio, (where that asset has a correlation of less than 1), will reduce the risk and volatility of the portfolio.

The potential portfolio benefit of adding alternative investments:

1. Less risk for same level of return, or

2. More return for same level of risk

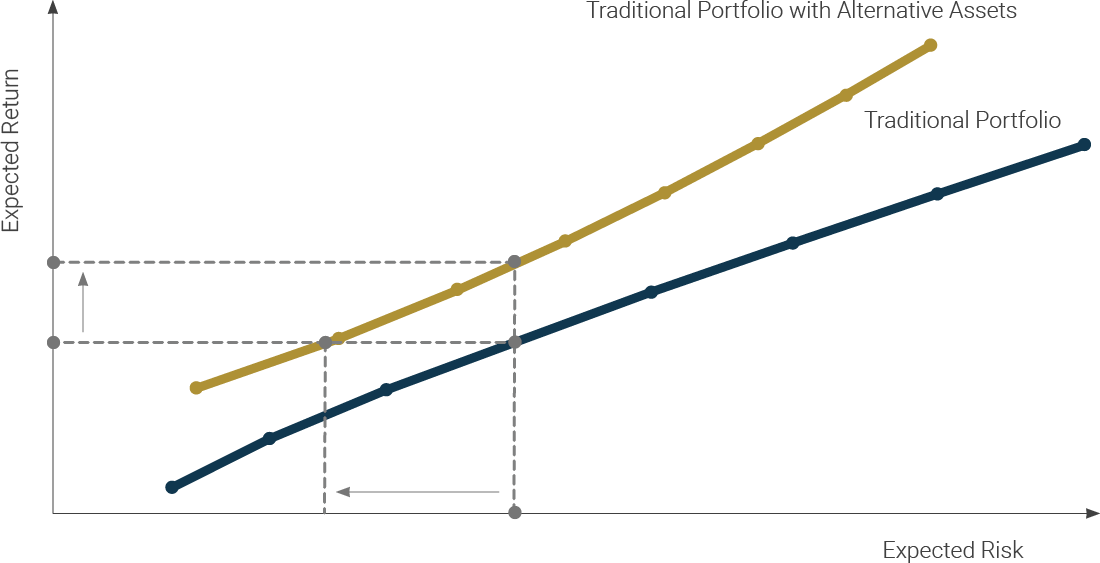

MARKOWITZ EFFICIENT FRONTIER

Source: Internal

Data effective July 1, 2010 (AIF Inception date) to June 30, 2021

The traditional Portfolio shows portfolio returns for the period indicated above for portfolios ranging from 100% Bonds to 100% Equities. The bond holding is represented by the S&P Canada Aggregate Bond Index and the equity holding is represented by a 50%/50% mix of the TSX and S&P 500.

In the traditional portfolio with alternative holdings, 20% of the portfolio is held as fixed in the DaVinci Capital Alternative Income Fund, with the balance ranging from 80% bonds, to 80% equity, as represented by the same instruments as in the traditional portfolio.

And finally, while we tend to focus on the risk management benefits of alternative asset classes, alternatives can often be a strong source of return as well as an alternative source of income. Given that alternatives are not as widely held as traditional asset classes, the opportunity to find alpha is greater, as mispricing doesn’t get arbitraged away as quickly as it does in public markets. While securities in public markets are well covered and analyzed by many buy and sell-side analysts, alternative asset classes often have less coverage and are less understood. Alternatives also tend to be less liquid, creating buying opportunities at a significant discount to intrinsic value.

Ultimately, alternatives assets provide additional sources of total return, but more importantly, allow an investor to properly diversify beyond just stocks and bonds to create a smoother return profile for their portfolio.

In fact, they are. The size of the market globally is now estimated at $7.7 trillion. Large institutional investors like Pension funds and Endowments, have embraced alternatives for years and continue to add to their allocations to try to improve investment performance. Family Offices have also been long time investors in alternatives. Private client investors have been constrained from embracing alternatives due to administrative and regulatory factors, but nevertheless private clients, especially the high net worth group, are gradually starting to increase their exposure to alternative asset classes, and strategies, as they too are seeing the benefits of taking a more sophisticated approach to investing.

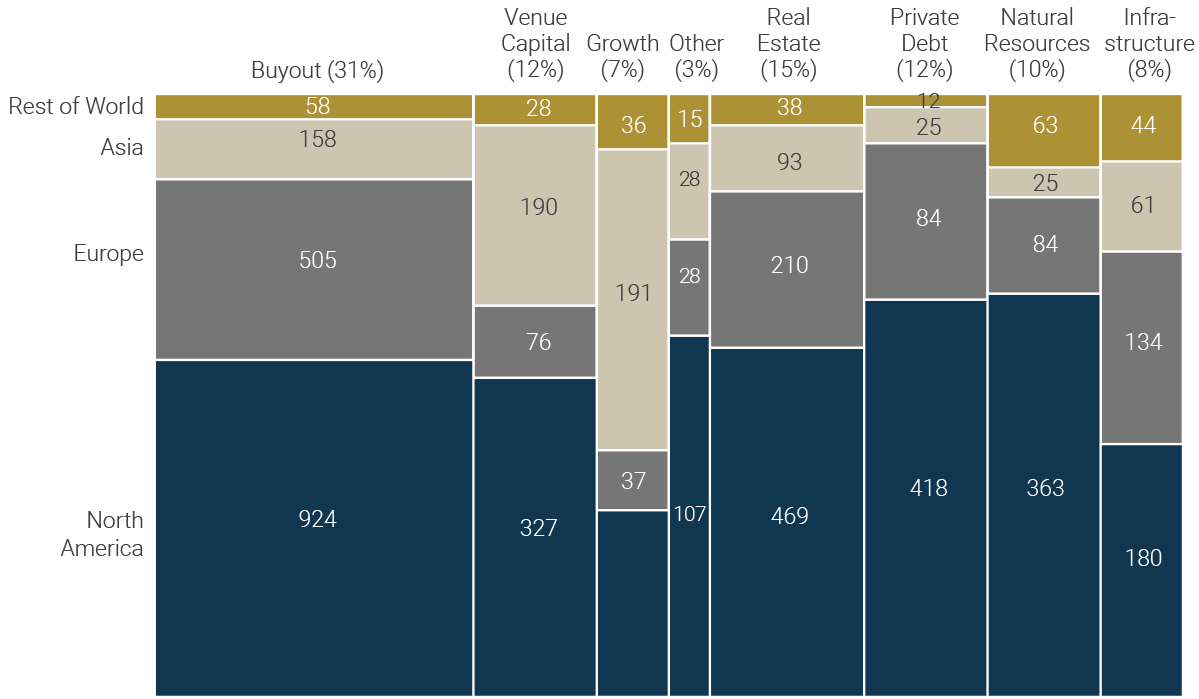

PRIVATE MARKETS LARGER THAN MANY OF US KNOW

$5.2 Trillion Assets Under Management, 2017, $ Billions

Source: Preqin; McKinsey analysis

HARVARD ENDOWMENT FUND – LONG TERM RETURNS

The value of $25,000 invested in the Harvard endowment has significantly outpaced both Canadian equities and a Global 60/40 mix of stock and bonds over the same time period.

Source: Harvard Crimson; Internal

| ASSET CLASS | STRATEGIC ASSET ALLOCATION |

|---|---|

| Public Equity | 27% |

| Private Equity | 20% |

| Hedge Funds | 32% |

| Real Estate | 8% |

| Natural Resources | 4% |

| Bonds/Inflation-Linked Bonds | 5% |

| Other Real Assets | 2% |

| Cash & Other | 2% |

| TOTAL | 100% |

Source: Harvard Crimson

The Strategic Asset Allocation mix

has 63% in alternative asset classes,

or non-traditional public securities.

Adding alternatives to your portfolio gives several potential advantages with respect to increasing return and

reducing risk:

RETURN

- Generate higher portfolio income

- Generate higher total returns

- Ability to be more opportunistic

during market dislocations - Greater opportunity for Alpha

RISK

- Reduce portfolio volatility

- Hedge against different economic risks

- Reduce portfolio drawdowns